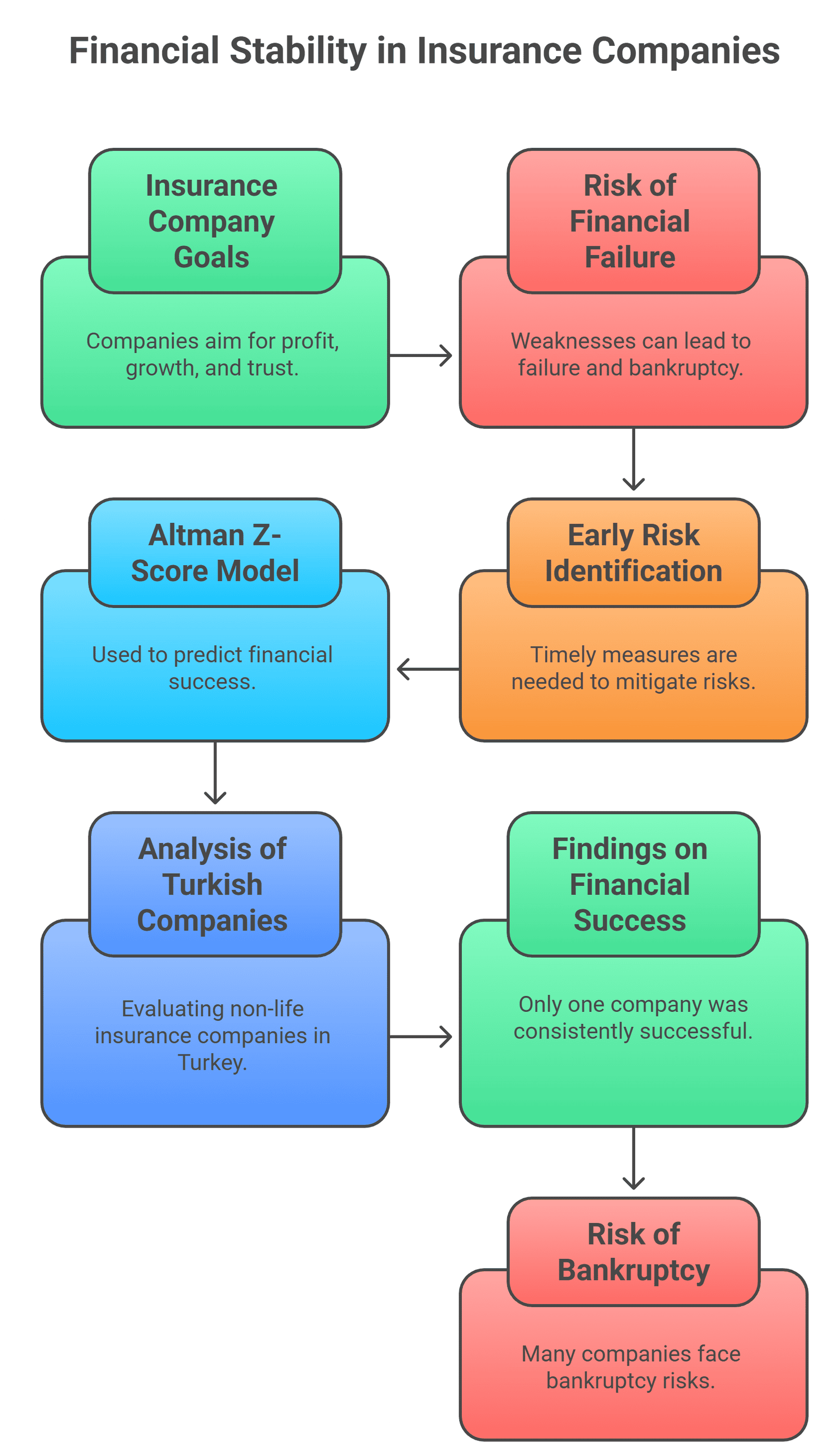

Insurance companies operate with the aim of generating profit, growing, and establishing trust in the sector in order to sustain their existence. Achieving these goals depends on companies having a sustainable and sound financial structure. Insurance companies with weaknesses or fragility in their financial structure, or those showing signs of such weaknesses, are more likely to experience financial failure, which in some cases can lead to bankruptcy. Therefore, identifying potential negative factors that could lead to financial failure at an early stage and taking necessary measures in a timely manner is crucial for reducing or completely eliminating the risk of failure. In this context, regular financial analysis and measurements that contribute to the current and future decision-making processes of insurance companies must be performed periodically. This study attempts to predict the financial success of non-life insurance companies operating in Turkey. The research focuses on financial failure prediction models and uses ten years of financial data covering the period 2014–2023. The Altman Z-Score model was applied by calculating the companies’ annual financial ratios, thereby assessing each company’s probability of financial failure. According to the findings, among the companies analyzed, only one company was financially successful throughout the entire period, two companies showed financial success for five years, while twelve companies failed to achieve financial success in any year during the ten-year period examined. This situation indicates that these companies are at risk of bankruptcy and that uncertainty prevails across the sector. For companies whose financial success status was determined to be uncertain, it is considered useful to conduct additional analyses using alternative financial failure prediction models (e.g., logit, probit, or machine learning-based approaches) to evaluate the current findings in greater depth.

Şentürk Y. Predicting financial failure of non-life insurance companies in Turkey using the Altman Z-score model, Res. Des. 2025; 2(2): 125-138. DOI: http://dx.doi.org/10.17515/rede2025-011ec0907rs